The problem almost never shows up on the day of the sale.

The customer takes the product, promises to pay later, and you scribble it down in a corner of a notebook or on a scrap of paper, send yourself a message, or think, "I'll organize this later."

A few days go by. Business still looks good: the store is selling, products are moving, the customer comes back.

And even so, cash gets tight.

That is when the uncomfortable question shows up: if I made the sale, where did the money go?

In a lot of stores, the answer is in pay-later control. Selling on pay-later terms is not the problem. The problem is pay-later control when it slips because of small, repeated, quiet mistakes. The money does not disappear all at once. It leaks out through improvisation.

The good news is that this kind of leak almost always leaves a trail. And once you learn to spot the mistakes, it gets much easier to fix the process without fighting with customers and without stopping sales.

Why tracking pay-later sales prevents you from losing money

Pay-later sales almost never break a business overnight.

They wear down cash flow little by little. That happens both in stores using a notebook and in stores trying to improvise a digital pay-later system without a clear routine.

A partially written amount, a promised payment date that never got recorded, a collection message sent too late, a customer who already owes more than they should and nobody noticed, one agreement lost in WhatsApp and another one kept "in your head."

Separately, each one sounds small. Together, they leak cash: the store keeps selling, but part of the money does not come in at the pace it should.

That is what makes pay-later sales confusing. The problem does not look like a problem at first. It feels like one.

- "I don't know where my money went."

- "The month was good, but less cash was left over than I expected."

- "I have customers who owe me, but I can't even say for sure how much is still open."

When that happens, selling on pay-later terms is not the mistake. Treating it like an informal favor, with no record, no due date, and no routine, is.

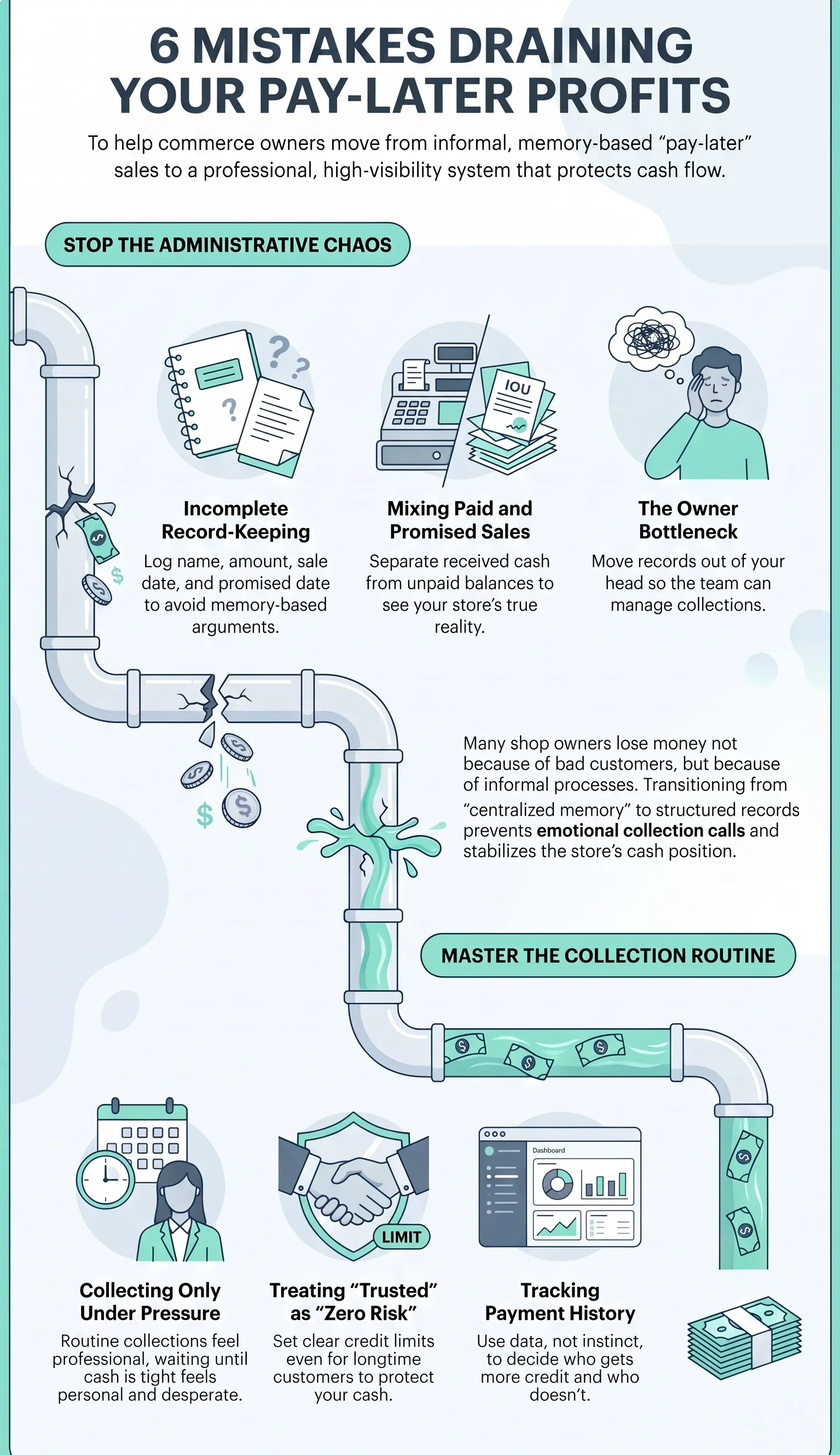

7 mistakes that make you lose money with pay-later sales

Mistake 1: Recording pay-later sales without a full date, amount, and agreement

This is the most common mistake and, at the same time, one of the most expensive.

The customer takes the product. You write down the name, maybe the amount, maybe not even that. The date stays implicit. The due date hangs in the air. The agreement stays in the conversation.

In the moment, it feels like enough.

Later, it turns into uncertainty.

When you try to collect, you no longer remember clearly:

- how much is still open

- what day the sale happened

- what due date was agreed on

- whether the customer was going to pay all at once or in parts

That kind of gap weakens the collection message. You sound less confident because you do not have full confidence in the record either.

And weak collection usually turns into longer delays.

The minimum for any pay-later process to work well is to record:

- customer name

- exact amount

- sale date

- promised payment date

- a short note, if there was an exception

It sounds basic, because it is. But that basic structure is what keeps your pay-later system from turning into an argument about memory later.

Mistake 2: Mixing pay-later sales with paid sales in the same control

A lot of stores throw everything into the same place: paid sale, unpaid sale, partial payment, customer note, loose observation.

The result is a mess.

When everything goes into the same flow with no separation, you lose the answer to two critical questions:

- What has already become cash?

- What is still open?

Without that separation, the owner looks at sales activity and thinks the store sold more than it actually collected. That is where many owners start thinking: "I'm selling, but I don't know where the money is."

Pay-later sales need to be visible as their own category inside your control.

Paid sale is one thing.

Sale on credit is another.

As long as those two situations stay mixed together, the store's cash position will look better on paper than it does in reality. And that gets in the way of everything: buying inventory, reordering, paying suppliers, and staying calm at the end of the month.

Good sales control starts right here: separating revenue from cash received.

Mistake 3: Not setting a limit per customer

One of the most dangerous habits in pay-later sales is treating "longtime customer" as if it meant "zero risk."

It doesn't.

A familiar customer can still be a great customer. But that does not eliminate the need for a limit.

Without a clear cap, the balance grows through improvisation. Today it is a small amount, then another item gets added, then one more exception. By the time you notice, that "trusted" customer has already built up a balance that weighs on your cash flow and feels awkward to collect.

A limit protects the relationship and the cash position because it prevents two things:

- exposing the store to a balance larger than it can absorb

- making collections emotionally harder once the balance has already grown too much

Even a simple limit improves the operation a lot. It can be based on:

- payment history

- purchase frequency

- average ticket size

- the store's real ability to absorb delays

When none of that exists, pay-later control stops being a business strategy and turns into uncontrolled accumulation.

Mistake 4: Letting collecting payments depend on memory

If collections depend on you remembering, they are already weak.

This is the point where many store owners realize the problem is not the customer. It is the process.

The owner remembers to collect when:

- cash gets tight

- they run into the customer by chance

- they see the name in WhatsApp

- they open the notebook and find the old entry

In other words: they do not collect when the payment is due. They collect when they happen to remember.

And that changes the tone of the collection.

Collecting on the due date feels normal. Collecting randomly, weeks later, feels personal.

That is how the whole thing becomes more uncomfortable than it needs to be. Collecting is not the problem. Collecting without a visible rule is.

A simple routine solves a big part of that:

- review open pay-later balances on fixed days

- look at that week's due dates

- send the collection message inside the agreed timeframe

When collections become part of a routine, they stop being an emotional impulse and become a normal part of the operation.

Mistake 5: Only collecting when cash gets tight

This mistake is an extension of the previous one and changes the tone of the relationship.

Some stores go for weeks without mentioning the balance. Then cash gets tight.

At that point, the collection message comes out loaded. Not necessarily in the words, but in the energy behind them.

Customers notice when a message is driven by urgency, irritation, or pressure. And that wears down even long-term relationships.

Collecting only when the store needs money creates two bad effects at once:

- you collect late

- you collect worse

The customer who could have paid calmly within a clear routine now gets a message that feels improvised, almost like the store is scrambling to chase money down.

Professional collections usually feel more human than improvised collections.

When there is a date, a record, and a clear agreement, the message stays professional:

"Hey, [name]. Just checking in about the amount we agreed on for today. If you need it, I can send the details."

When there is no process, the message carries emotional weight.

Disorganized pay-later sales weigh on cash flow and on the conversation itself. In the U.S., the same kind of pressure shows up in small businesses whenever cash timing slips and collections become reactive instead of routine.

Mistake 6: Not tracking the customer's payment history

Without history, every customer looks the same. And that gets expensive.

In real life, there are very different profiles:

- customer who always pays on time

- customer who is slightly late but gives you a heads-up

- customer who only pays when reminded

- customer who disappears and takes more energy to collect from

When you do not track that behavior, you keep making decisions by instinct:

- who can buy again

- who deserves a longer term

- who is already at the limit

- who needs a tighter rule

That is the point where pay-later sales stop being management and turn into guesswork.

The history is not there to punish the customer. It is there to improve the store's decisions.

With it, you stop treating credit like an emotional call and start treating it like a relationship with memory.

A customer management record showing what the person bought, how much is still open, and how they usually pay gives you much clearer visibility into who owes, how much they owe, and how they tend to pay.

Without that history, store owners often reward the wrong customer and hold back the right one.

Mistake 7: Keeping the whole system in the owner's head

If only you know who owes, how much they owe, and when they were supposed to pay, your store does not really have a process. It has centralized memory.

And centralized memory breaks fast when:

- volume grows

- someone else joins the team

- you need to step away

- WhatsApp turns into a maze

This mistake weighs especially heavily on owners who already handle everything. Pay-later sales become one more responsibility that depends entirely on them. One more thing nobody can touch without asking. One more operational detail draining mental energy.

The problem is that, as long as control lives only in the owner's head, the store cannot:

- delegate collections

- keep registration consistent

- respond quickly

- scale without adding chaos

When only the owner knows everything, any day off, illness, trip, or unusually busy week becomes operational risk.

At that point, pay-later sales stop being a commercial practice and turn into a personal bottleneck.

How to fix pay-later tracking mistakes without stopping pay-later sales

The way out is not to kill pay-later sales overnight.

In many local businesses, selling on pay-later terms is part of the trust built with repeat customers. The mistake is not the practice itself. The mistake is failing to give it structure.

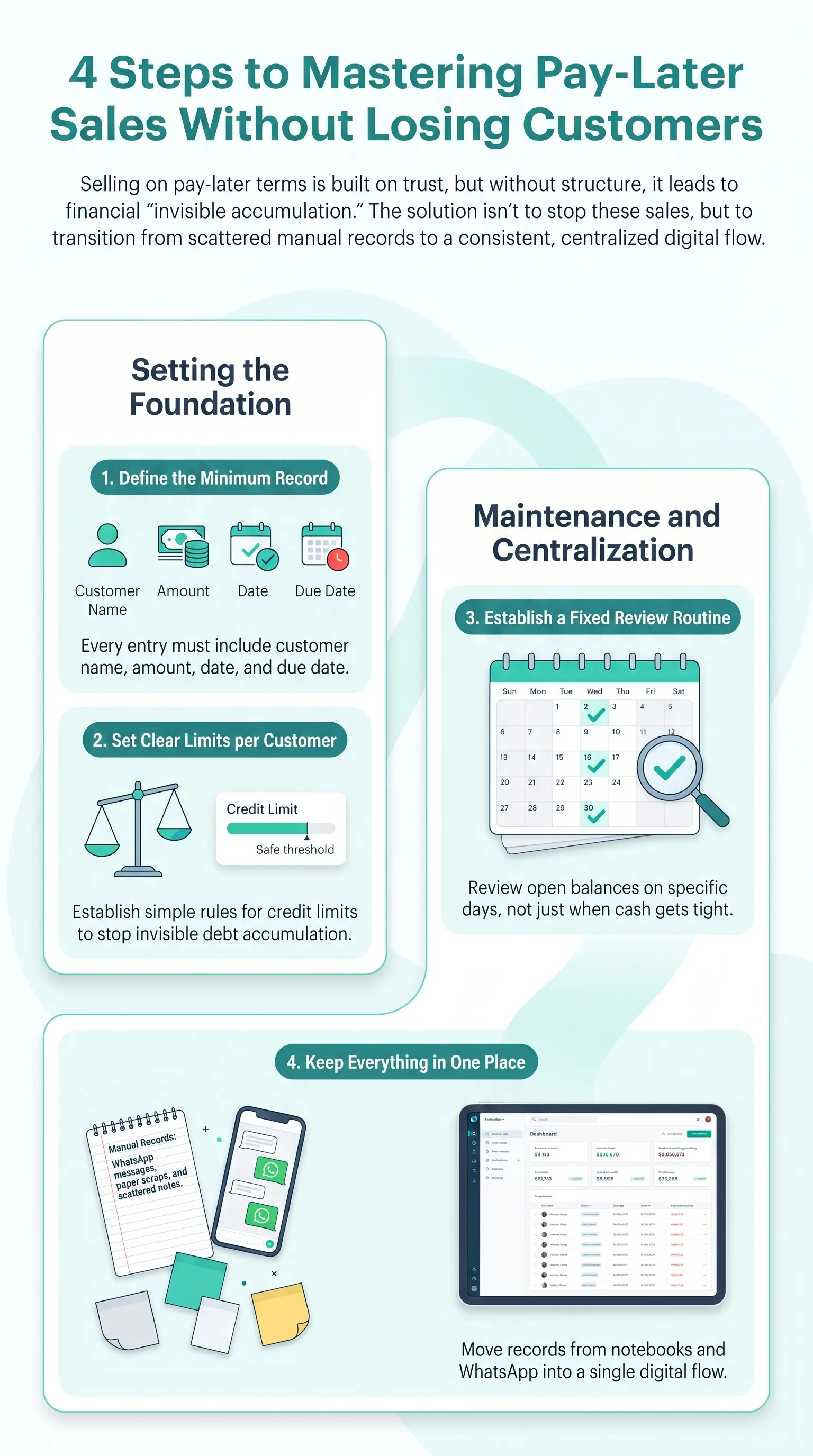

Four simple steps already improve the situation a lot:

1. Define the minimum record required

No pay-later balance should exist without:

- customer name

- amount

- date

- due date

Without that, there is no control. There is only a partial memory.

2. Create a limit and a due date per customer

You do not need to overcomplicate it. Start with a clear rule that is easy to apply. The goal is not bureaucracy. The goal is to stop invisible accumulation.

3. Have a fixed review routine

Pick specific days to look at what is still open. That keeps collections from happening only when cash gets tight.

4. Keep everything in one place

When part of it is in a notebook, part is in WhatsApp, and part is in your head, the process is already broken. The first gain from tighter control is bringing everything into one organized system. That is the point where many stores start replacing the notebook with a more consistent digital pay-later flow.

When pay-later control needs to move out of the notebook

The notebook did not appear for no reason. It exists because it is fast, familiar, and seems good enough when sales volume is still small.

The problem is that it handles the counter better than it handles the end of the month.

In general, it makes sense to move on from the notebook when at least one of these situations shows up:

- you can no longer remember everything confidently

- there is more than one customer conversation channel

- someone else on the team needs to check balances

- the open balance has started to weigh on cash flow

- collections have become too uncomfortable

At that point, the issue stops being "write it down better" and becomes "get pay-later sales out of improvisation." In other words: move out of the notebook and into a digital pay-later routine that protects the relationship without sacrificing cash flow.

Conclusion

Pay-later sales do not destroy a store all at once. They wear the business down like a small leak. And everything keeps looking normal until cash gets tight.

Incomplete notes, late collections, poorly defined limits, missing history, and dependence on the owner's memory create a dangerous package. That does not point to bad intentions. It points to missing process.

Having a process does not mean becoming cold with customers. It means being able to offer pay-later sales without losing control. It means having pay-later control that still works when volume grows, WhatsApp fills up, and cash gets tight.

If your store is already feeling that weight, the next step is to organize the operation. A digital control system with customer history, limits, records, and WhatsApp support helps get pay-later sales out of the notebook, strengthens pay-later control, and brings the money back into the store's line of sight.

Frequently asked questions

Is selling on pay-later terms always a bad idea?

No. In many businesses, pay-later sales help maintain relationships and repeat purchases. What hurts the store is not pay-later sales themselves. It is the lack of control.

How do you collect a pay-later balance without making the customer uncomfortable?

The best way is to collect inside a predictable process. When there is an agreed date, a recorded amount, and a routine, the collection becomes more objective and less personal.

How do you define a limit per customer?

Start by looking at payment history, purchase frequency, and the impact a delay would have on your cash flow. A good limit protects the sale without exposing the store too much.

When should you stop tracking pay-later sales in a notebook?

When the notebook no longer tells you clearly who owes, how much they owe, and when it is due. If you need memory to fill in the missing pieces, you are already past the point where you need to reorganize.